.jpeg)

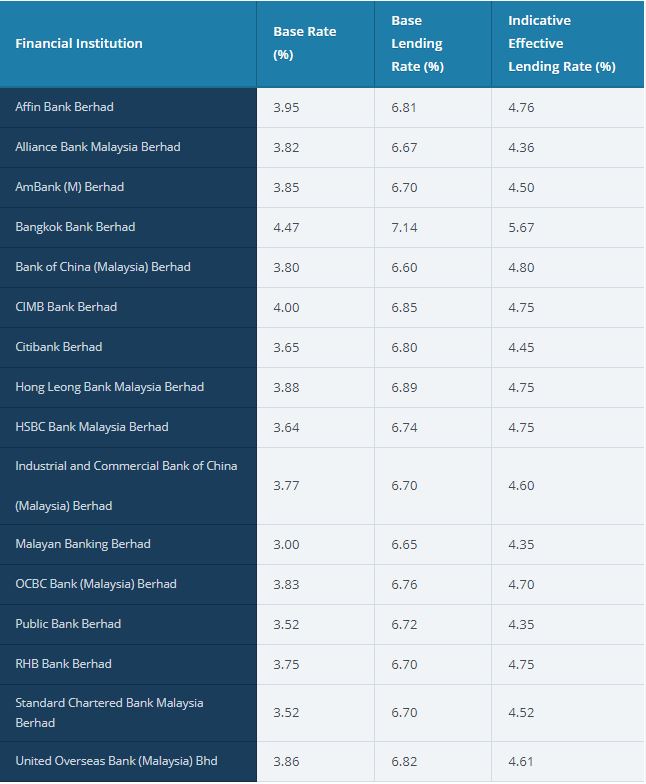

In January 2015, the Base Lending Rate (BLR) structure was replaced with a new Base Rate (BR) system. Under BR, which now serves as the main reference rate for new retail floating rate loans, banks in Malaysia can determine their interest rate based on a formula set by the central bank.

Under the previous BLR, the rate was set by Bank Negara Malaysia (BNM) based on how much it costs to lend money to other financial institutions. Meanwhile, the cost to borrow money was determined by the Overnight Policy Rate (OPR) set by the central bank.

With the new BR, which came into effect on January 2, 2015, interest rates are determined by the banks’ benchmark cost of funds and Statutory Reserve Requirement (SRR). Other components of loan pricing such as borrower credit risk, liquidity risk premium, operating costs and profit margin will be reflected in a spread in the new BR framework.

Why the change?

Instead of a fixed rate under BLR, BR is determined by banks without intervention by the central bank and should differ from bank to bank depending on their own efficiencies in lending. Banks with a strong niche in consumer financings such as Maybank and Public Bank will have the initial edge of being able to offer more attractive and competitive BR and effective lending rates (ELR) for their customers.

The new framework encourages greater transparency from banks and will enable customers to make better financial decisions. Previously, calculations of BLR lacked transparency and some banks were lending below the BLR to attract customers and boost loan growth. Under the new system, customers cannot borrow below the base rate.

Source: BNM

Figures are accurate as of June 2019

.jpeg "Sidebox")