.jpeg)

The world we knew, joyful, very social and with a conducive property market, suddenly disappeared in March 2020 and the 2020 year’s end, because of the pandemic, will be remembered as the less happening of the past 100 years, or more.

No big parties and celebrations and not many fireworks either, in general, a cautious and “socially distanced” approach towards the New Year, together with a fear that property market might be crashing soon if a new surge of the pandemic will kick in!

Healing Of Property: A New And Different Market

Property industry, which was already suffering from a high “unsold stock” before the pandemic kicked in, has definitely taken a bad hit!

The Covid-19 pandemic has contributed to worsening the property market perception about “investment”, and specifically property investing or buying, resulting into a negative result for 2020!

However, being able to look at all the above happenings with a positive eye, the current global situation is presenting, to all of us, “the greatest opportunities of the past 100 years”!

Let’s go together through the main trends detected in the property market to get where, in the months to come, the good opportunities for property hunters will be. To get ready for the future, we must first analyse the past!

Property Pain Points From The Past: The Pre-pandemic

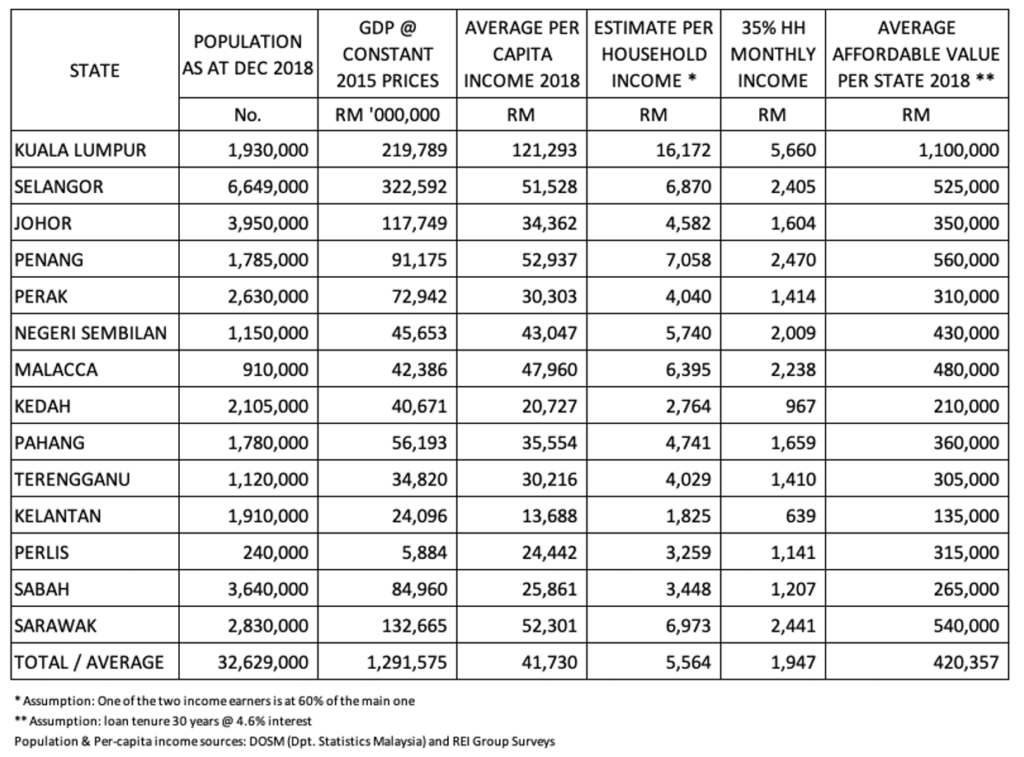

Residential market in Malaysia, since the beginning of the 2019, has been showing a growing demand toward both landed and high-raise properties priced below RM700,000 (USD175,000), for some areas of Malaysia the value to be looked at is RM400,000 (USD100,000).

City Centres properties, not only in Kuala Lumpur, have been left aside, by potential buyers, due to the high cost per square foot, sizes either too big or too small and, above all, due to the huge unsold stock which, combined with low occupancy rates (untenanted units), clearly shows a substantial over supply situation.

Office market in 2019 was already having an impressive quantity of unoccupied space. Several big projects in both Kuala Lumpur and Johor Bahru, were in the process to make the situation even worst by delivering millions of square foot of new office space between the end of 2019 and 2020!

Retail properties and industry witnessed the raise of e-commerce which have been start pulling away from malls “real shoppers” transforming them in pure shopping mall pass-byers with a tendency to try and test purchasable items in the mall and then go home and order them online.

Besides few renewed malls, those having established their brand since long such as MidValley or KLCC Suria just to mention two, the majority of new shopping mall, in 2019, were already suffering for lack of crowd and consequently poor occupancy.

Talking about numbers, Malaysia has the highest square footage of retail space per person (out of the whole population of the city where the shopping mall is) in the whole of South East Asia, something to be considered when a developer will be thinking about developing a new mall.

Resorts and hotels, around Malaysia, managed to hit occupancy rates below 65% in 2019. Malaysia, unfortunately, has not yet been able to become enough sexy and appealing to “repeated visitors” and “long-term” tourists. Building owners, developers and operators were all hoping for a better 2020!

Loan approvals for properties, in December 2019, were at the lowest with most of the few approved mortgages, at far below the previously commonly granted 90% margin of financing.

Property developers were requesting Bank Negara to partially release the curbing measures, introduced in the previous years to moderate or eliminate speculation, to ease the disposal of unsold properties. The government and the developers’ associations were also discussing the possibility to extend the Home Ownership Campaign (HOC) to 2020.

The Covid-19 Pandemic Strike!

Then Covid-19, the pandemic, stricken causing the Great Lockdown to kick-in and social distancing and WFH to become part of our “New Normal” lives!

From a residential point of view, the demand for bigger spaces, at least from the 70% of Malaysian professional adopting the WFH mode, is on the raise as far as the “expansion” of the search-range for properties to sub-urban and beyond areas.

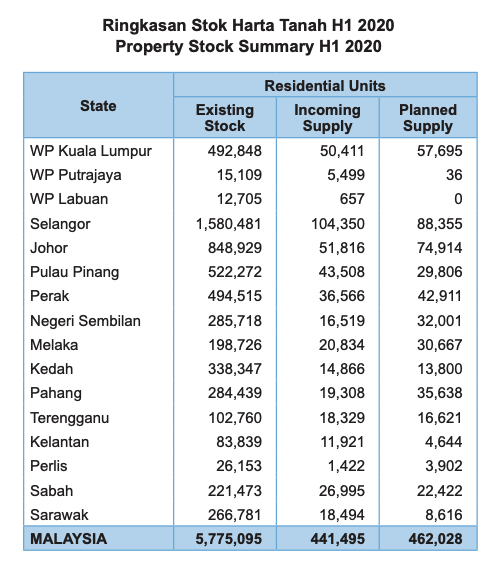

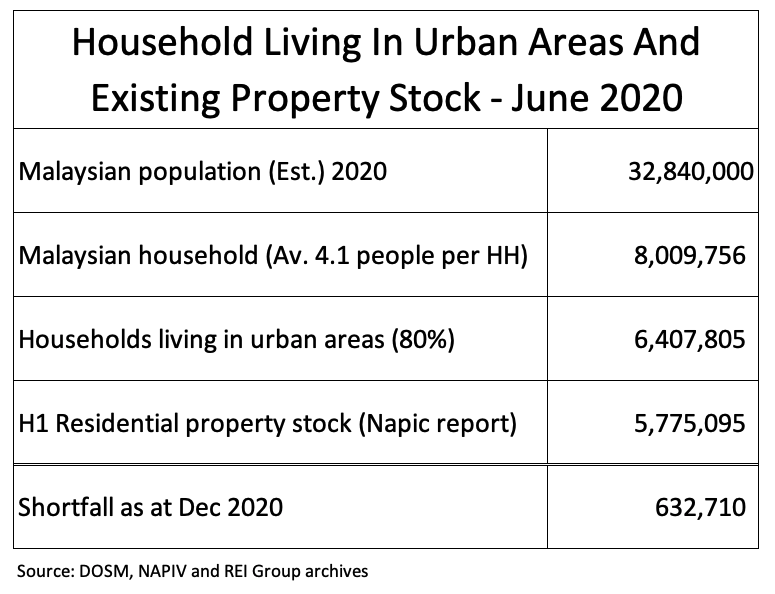

Furthermore, recently released data from NAPIC are confirming that the supply (for values below RM700k) is still behind the potential demand, when compared with demographic data (check these two tables comparing existing stock of properties with total number of household and you will get it).

Families currently living in limited spaces, below 700 sq.ft., are on the search for bigger properties where a wider space or even a dedicated room could be allocated to “WFH-area”.

The “sexy-of-the-past” studio unit might not anymore be as a popular property as it was in the past and, even worst, it will not be possible to recycle it into AIRBNB or short-staying for tourists. Tourist arrivals is still and will remain for quite some time a fairy tale thanks to the pandemic!

The so popular TOD (Transit Oriented Development), small studio units within high density buildings incorporating a public transportation station, might be left empty with the “WFH mode so I need more space” being the killer once more.

In general, we can expect the past property “up-zoning” trend (high density within urban areas) to move towards “down-zoning” (low density development, low raise or landed properties and away from city centres).

Property primary market still offers great opportunity and more will come our way in the forthcoming future. The Malaysian Property Market will definitely recover, raise and shine as never before but it might be taking a while.

In the meantime, better get ready to grab the good opportunities which will come our way following the table below for the “buy” or “don’t buy” decision.

Hot spots wise, Greater KL, its sub-urban and beyond areas still remain a good choice. For better understanding, the beyond covers the “West and South Corridors of Klang Valley” respectively till Port Klang and Seremban.

Johor Bahru and Iskandar Malaysia, property wise, are still representing a good buy providing the investor, during these trying times, has good holding power. A comparative parallel with Shenzhen shows that, eventually, it will happen. It is just a matter of keeping in mind that Shenzhen was launched in the middle ’80s and it took more than 30 years to become an “economic region and property” success story.

Penang, Malacca, Kota Kinabalu and Sarawak are also still a good destination for property investors, providing due diligence is done on the market trend and related demand which are very different location wise and for sure considering the “long wave effect” of then-current pandemic.

To be kept in mind, while doing the due diligence on a possible property investment, to always double confirm all the given information by the sales representative to make sure everything is correct!

Upcoming star in the property investment panorama is Kuantan. The main city and commercial harbour of the east coast of Malaysia, Kuantan is raising its attraction due to the upcoming ECRL (East Coast Rail Line) and all the happening, in terms of industrial parks development, driven by the ECER (East Coast Economic Region) planning.

Some very interesting townships have been and are growing with property developers delivering products which for once are demand-driven! Worth paying a visit!

What will happen with all those millions of empty property square feet from office, hospitality and, eventually, retail then? Recycling and reusing will be the passwords!

Malaysia has still a substantial shortfall of affordable housing and empty office and hospitality space might be partially re-developed to address this demand. It is a medium-term game but could be working. Another very interesting niche of the property market that few have been looking at, is the fast-growing group of aged Malaysians.

In the next 20 years the “third age group” (people aged 65 years and above) will almost double while the natural grow rate for Malaysia, will keep on remaining stable. Result is, higher demand for “residential-cum-medical-care-services” properties and several resorts and hospitality designed building, would be perfect to address this demand.

In conclusions, Malaysia has and is surviving the “2020 Perfect Pandemic Storm” pretty well, we know when it started but cannot foresee, for the moment, when it will end but, like all the storms it will end, and sun will shine again better than before, eventually!

The above are just some ideas or thinking points for the readers about property, pandemic and the future. If you have more, agree or eventually disagree and want to reach the author, he will definitely reply to your comments.

This article was written by Daniele Gambero and originally published on Prosales.

.jpg)

.jpeg "Sidebox")