.jpeg)

As Malaysia's central bank, Bank Negara acts to promote monetary and financial stability and ensures that we have a strong financial sector that supports the nation's economic goals and objectives.

The central bank also plays a significant role in ensuring all economic sectors and segments of society have access to financial services. One of the most watched or a sector that has significant multiplier impact to the economy is none other than the property sector.

To educate the general public or stakeholders and to ensure that all information with respect to the housing market is collated, Bank Negara runs a website under www.housingwatch.my which basically provides a wealth of information on the state of the Malaysian housing market.

Recently, the second quarter data for 2018 was uploaded onto the website and key findings include on financial performance of Malaysia's housing market. According to Bank Negara, the total outstanding housing loans in the banking system grew by 8.3% as at end of June 2018 and the approval rate for house buyers remained strong at about 72.1%.

In terms of the composition of house buyers, 71% of housing loan borrowers were first-time owners of properties priced below RM500,000 with 49% of them in the "below RM250,000" and 22% in the "RM250,000 and RM500,000" categories.

While the above statistics do tell a story, there is another story being told via Bank Negara's monthly statistical bulletin, which is typically released at the end of each month for statistics related to the preceding month.

In the latest update for August 2018, it highlighted that the total loans outstanding for the purpose of purchasing residential property in the banking system stood at RM545.6bil and this makes up one-third of the total banking system loan of about RM1,641.2bil.

The banking system itself experienced a loan growth of about 5.4% year-on-year (y-o-y) in August 2018 while loans extended for the purpose of purchasing residential property expanded at a much faster pace of 8.2% y-o-y.

Bank Negara also provides statistics on the banking system's loans applied and approved, both by purpose and by sector respectively. Here, dissecting the data further it shows that for the month of August 2018, loans applied in the banking system for the purchase of residential property amounted to RM24.3bil, up 2.9% y-o-y but down 0.1% m-o-m. Cumulatively, the total loans applied for the purchase of residential property year to-date stood at RM161.3bil, up just 0.3% y-o-y.

On loans approved, the data showed that for the month of August 2018, loans approved were just RM9.73bil, which was 7.1% higher m-o-m but lower by 0.8% y-o-y. Cumulatively, the data showed that total loans approved year-to-date stood at RM67.23bil, relatively flat compared with RM67.24bil a year ago.

From here, we can summarise another interesting statistic which is the percentage of loans approved against applied in value. For the month of August 2018, the percentage translated to 40.1%, which is an improvement of 2.7 percentage points compared with the July 2018 figure of 37.4%, but still lower by 1.5 percentage points when measured against last year's August figure of 41.6%.

Cumulatively, the year-to-date approval rate is now at 41.7% against 41.8% for the same cumulative period in 2017.

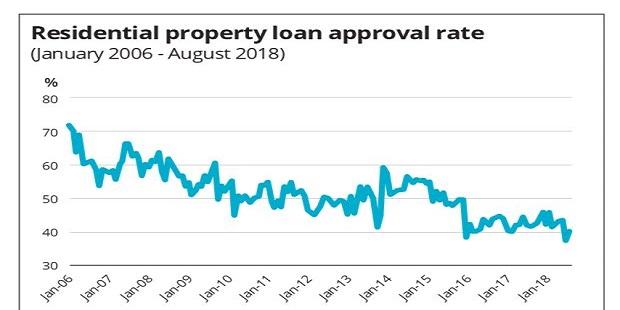

The chart shows that based on the data provided by Bank Negara, we can derive the banking system loan approval rate for the purpose of purchase of residential property based on the total loans approved against applied on a monthly basis. Here, the assumption is that what is applied in the current month is deemed as being approved in the same month although in reality this may not be the case, as banks may take more than a month to approve an application.

In addition, if a loan is applied later in a particular month, it is obvious the approval will likely be in the following month, the earliest. Nevertheless, the monthly approval figure do take into account the preceding or previous month's applications and hence on a net basis, the actual approval rate may not run that far against what is captured from this data.

We can see that loan approval rate has been deteriorating over time. Even during the Global Financial Crisis of 2008 and 2009, loan approval hovered at 59% and 54% respectively. Are the current batch of loan applicants that bad to the extent loan rejection (based on value) is so high and approvals are at low 40%? The above chart also showed that loan approval rate used to hover even at high 70% in early 2006.

Bank Negara in its housing watch website cited three key reasons why loan applicants get rejected and they are mainly due to lack of residual income after taking into consideration other obligations, poor track record among borrowers as well as insufficient documents to support the ability to repay the applicant's loan obligation.

What is telling from the above data is that while the central bank has dispelled the property market players' argument that loan approval rate is low by explaining that approval rate is at 70% and above, the actual data that is shown in the monthly statistical bulletin shows loan approval based on value is just at about 41%-42%, which basically is more supportive of the argument brought by developers.

Could it be that the data provided by Bank Negara on approval rate is based on the number of applicants and not value, or is it the 70% plus approval rate only refers to first-time buyers? We need to shed more light on the actual data before we can formulate strategies to allow greater flexibility in housing loan approvals.

.jpeg "Sidebox")