.jpg)

_PH_Banner_(Desktop)(1200x180px).png)

.jpeg)

If you're still financially able to, there are 3 options for you to consider: rescheduling, restructuring, or debt consolidation. However, if you find yourself struggling, there's still a last glimmer of hope.

.jpg)

With a lot of uncertainty regarding the future, COVID-19 brought not just health and safety issues, but also the loss of employment, businesses closing down, and an extra financial obstacle to tough out in the rat-race of life.

To assist businesses and individuals financially affected by the pandemic, an automatic deferred loan/financing repayment was introduced by Bank Negara Malaysia (BNM), beginning 1 April and slated to end on 30 September 2020.

Commonly known as a loan moratorium, it was a hopeful message for many struggling during the Movement Control Order (MCO), as they would be able to defer loan repayments until their finances had stabilised.

However, one small drawback of the moratorium was that it led to higher repayment amounts because of the accumulated interest for your home loan (the decision to compound interest was later removed by all major banks).

But! The moratorium also provided a huge financial relief for those facing retrenchment or suddenly out of a job, as they could focus on more crucial things like food and face masks.

So, now that things have pretty much stabilised and we’re in recovery mode, our question is...

What Happens After The Moratorium?

As we now try to adapt to the new normal, the government has announced that banks will continue to provide targeted moratorium extensions and flexible loan repayments, even after 30 September. What this means is:

1. An extension of the loan moratorium for another 3 months for those who have lost their jobs this year, and are still unable to find new employment.

2. A reduction in loan instalment proportional to their reduced salary (for those with pay cuts) for at least 6 months, with the possibility of another extension afterwards.

The banks have also agreed to provide repayment flexibility, bearing in mind the circumstances of the borrowers and whether they have been affected by COVID-19. They include:

• Permitting borrowers to make payment for only the interest portion of the loan for a certain period of time.

• Reducing monthly instalments by lengthening the loan period.

• Different options of repayment flexibility until the borrower is financially stable to resume their full repayments.

How Can I Manage My Home Loan Repayment After The Moratorium?

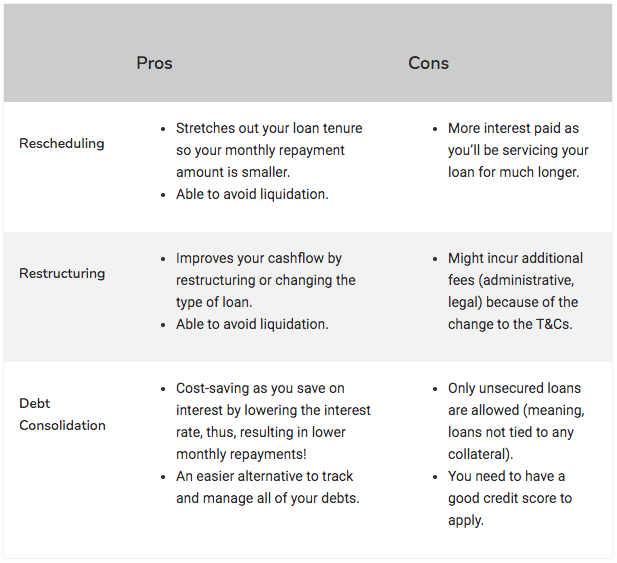

Once the moratorium is over, you’ve got 3 options to manage your repayments and debt for your property, if you still have the financial capability: rescheduling, restructuring, or debt consolidation.

Rescheduling provides you with an extension (longer time period) for financing/loan tenure, and a revision of instalment payments, where the main terms and conditions are significantly unchanged.

Restructuring means modifying the terms and conditions of your financing/loan principal to match your cash flow. This includes restructuring or converting the type of financing/loan, like going from an overdraft to term financing.

Debt consolidation is the third and final option. It involves you taking a new loan… to pay off your other loans. It sounds crazy, but here’s the good bit: you’ll get to clear allll your loans with just ONE interest rate!

Should you opt for either rescheduling or restructuring your property loan after the moratorium, the good news is that it won’t be recorded in your CCRIS report!

Additionally, banks like RHB and Hong Leong will hold special assistance programmes on selected days for their customers, namely:

• RHB Banking Group's loan and financing payment assistance clinics on September 19 and September 26 at more than 100 branches nationwide.

• Hong Leong Bank and Hong Leong Islamic Bank's “Advisory and Assistance Days” on September 19, September 26, and October 3 at all its branches nationwide.

What If I Really Can’t Repay My Home Loan?

If none of those work and you’re still finding it difficult to repay your loans, talk to the Agensi Kaunselling dan Pengurusan Kredit (AKPK) for some financial counselling, education, and to develop a personalised debt management programme for you.

Once that’s done, the next thing to do is to gather up your courage, call your bank soonest possible, and be honest with them about your current situation.

You won't be the only one facing this problem, so we’re pretty sure banks will be understanding and help you as much as they can.

However, the most important thing you should NOT do is: Completely ignore your loan repayments! It’ll drag your credit score down, you’ll be charged with extra penalties, and (worst case scenario) the bank can repossess your assets as well as file you for bankruptcy.

As such, try your best to plan your finances in advance so you won’t be left scrambling once the moratorium ends, so you'll have ample time to evaluate your next course of action!

.jpeg "Sidebox")

.jpg "Sidebox")