.jpeg)

_PH_Banner_(Desktop)(1200x180px).png)

The 2019 Real Property Gains Tax rates are a significant factor for consideration to anyone who owns a property and intends to profit from its sale.

The Real Property Gains Tax (“RPGT”) in Malaysia is definitely not a new subject for property owners – veteran investors especially. First introduced in 1995, the latest iteration of RPGT rates in 2019 are expected to dampen soaring prices with a tax imposed on any profit made from the sale (or “disposal” in financial parlance) of a property.

The RPGT is governed by the Real Property Gains Tax Act 1976 and is defined as a tax imposed on any “chargeable gain” of any “real property” or “chargeable asset” by “chargeable persons”. Now that you’ve been introduced to some of the jargon – this article will detail all you need to know about the Real Property Gains Tax.

What is RPGT?

In simple terms, RPGT is chargeable on the profit gained from the sale of a property, or shares in a Real Property Company, and is payable to the Inland Revenue Board of Malaysia (IRB) – the “taxman” also known as the Lembaga Hasil Dalam Negeri (LHDN). The “chargeable person”, or seller of a property, can be a resident or non-resident in Malaysia and even a company. The Act also includes those who sell a property in the capacity of a trustee, executor of a deceased’s estate, or guardians of a chargeable person.

The sale of both residential and non-residential properties will be levied with RPGT but it is crucial to take note that it only applies in transactions where a profit has been gained. For example, “A” first bought a property in 2015 at the price of RM500,000 and subsequently sold it to “B” in 2017 for RM750,000. A profit is gained in the amount of RM250,000 and will be chargeable with RPGT.

However, there is no need to pay for RPGT when:

1. The disposal price is lower than the acquisition price when the seller first acquired the property;

2. The disposal price is equal to the acquisition price when the seller first acquired the property.

In both of these situations, as no profit has been made, there would be no chargeable gain from the disposal of property.

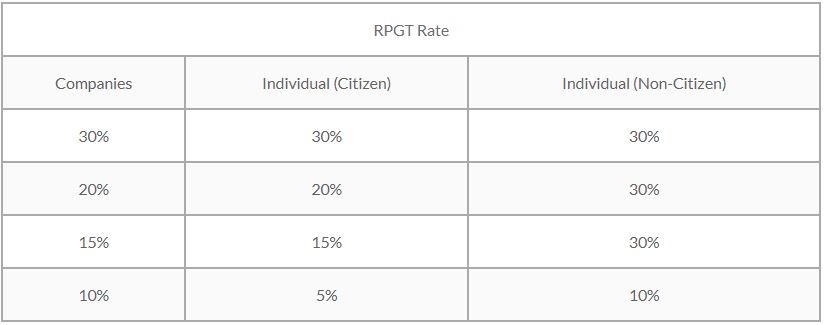

How do I Calculate RPGT?

The formula is rather simple. You simply apply the RPGT Rate to the chargeable gain. The current rates for RPGT (based on Schedule 5 of the Real Property Gains Tax Act 1976) are as follows:

Applying the example above, the disposal period of “A” would have been within 3 years (ie. from 2015 to 2017). Thus, 30% will be chargeable on the profit gained.

However, before we conclude the calculation, it is worth noting that the law does allow deductions on miscellaneous charges or any incidental costs incurred (according to Paragraph 6 Schedule 2 of Real Property Gains Tax Act 1976) from the profit gained as a result of the disposal of the property. These miscellaneous charges will include your legal fees, agent fees, stamp duties, and renovation costs.

When should I pay my RPGT?

Under Section 13 of the Real Property Gains Tax Act 1976, both the buyer and the seller will need to file a tax return to the IRB within 60 days from the date of the Sale and Purchase Agreement (or the unconditional date) by filling “Borang CKHT 1A” (for the seller or “disposer”) and “Borang CKHT 2A” (for the buyer).

In practice, this will normally be done by their respective lawyers engaged in the property transaction, though the disposer or the buyer may elect to do this on their own. However, bear in mind that fines will be imposed for making late filings, incorrect calculations, or omission of details. If you are represented by a lawyer or tax agent, it is best to let them file the relevant forms for you.

It is also required under Section 21B(1) of the Real Property Gains Tax Act 1976 that the buyer’s lawyer retains 3% of the purchase price from the deposit paid and remits the same to the IRB together with the prescribed tax forms within the 60-day timeframe.

The lawyer will then submit the current and previous Sale and Purchase Agreement together with all the relevant documentation for the calculation of RPGT by the IRB. In return, a notice will be issued stating how much RPGT is to be paid by the disposer. In the event an excess has been paid, the IRB will make a refund to the disposer.

On the other hand, if there is a failure to pay the RPGT within the timeframe given, a 10% penalty will be imposed on the amount payable.

Further to the above, on 1st January 2018, the Finance (No.2) Act 2017 came into effect with amendments to the Real Property Gains Tax Act of 1976. Pursuant to the amendments, it is worth noting that if you are a foreigner wishing to dispose of a property, a sum not exceeding 7% must be retained by the purchaser’s lawyer for RPGT purposes.

Am I entitled for an exemption?

Under the Act, there are certain exemptions allowed for the disposer. The exemptions include:

1. Once-in-a-lifetime exemption for an individual, citizen, or permanent resident of Malaysia, for the disposal of a private residence. Each person will be entitled to apply for this exemption once in their lifetime – provided that the property is a residential property (Section 8 and Schedule 3 of Real Property Gains Tax Act 1976).

2. The first RM10,000 or 10% of the profit gained, whichever is higher (Schedule 4 of Real Property Gains Tax Act 1976). This came about after the Budget 2014 was tabled, where the RPGT was increased by the Government to reduce speculative activities in property dealings. Thus, the computation of the chargeable gain shall now include this exemption (i.e. Chargeable Gain = Profit Gained − [RM10,000 or 10% of profit gained, whichever is higher] − miscellaneous charges or incidental costs.

3. Transfer of property by way of a gift between family members. Family members shall include spouses, parents, children, grandparents, and grandchildren. Any other transfers apart from the said family members shall not be exempted. It is presumed under the Act that the transferor has not received any gain or loss from the transfer of the property and the disposal price shall be deemed to be equal to the acquisition price (Paragraph 12 Schedule 2 of Real Property Gains Tax Act 1976).

Therefore, it is wise to first weigh all the pros and cons and make the necessary calculations before making any decision to sell your property.

If you are not familiar with the formula of the RPGT rate or calculation, you may download the EasyLaw RGPT calculator app at easylaw.com.my or refer to professional lawyers and tax agents.

.jpg)

.jpg)

.png)

.jpeg "Sidebox")