.jpeg)

_PH_Banner_(Desktop)(1200x180px).png)

As 2019 gets under way, the general outlook for the local property market this year seems to be one of cautious optimism, with windows of opportunities for recovery in the mid to longer term.

In the residential market, Savills Malaysia executive chairman Datuk Christopher Boyd says values will continue to slide. Ultimately, he says the market within Greater Kuala Lumpur (KL) will recover first, followed by Penang, and then Johor.

"There are about 245,000 new residential units under construction in Greater KL, with about 55,000 units in Penang and 108,000 units in Johor. This supply pipeline means that supply of residential units will grow by 10% to 12% in the next couple of years.

"Prices will adjust to meet effective demand, but there will never be a remedy for building cheap houses in undesirable locations."

Knight Frank Malaysia residential sales and leasing associate director Kelvin Yip says market enquiries and activities have increased in spite of the challenging market environment currently.

"In 2019, we expect to see more motivated sellers and discerning buyers to be present in the residential market. Various policies announced in Budget 2019, which are designed to aid first-time homebuyers, are also expected to kick-start the housing market moving into 2019 and beyond.

"Malaysia's residential properties will continue to be attractive in the eyes of foreign buyers as a result of our liberal policies, reasonable valuations and coupled with no extra stamp duties."

AllianceDBS Research however is less optimistic about the local property market this year, as it believes that the sector will continue to be plagued by the existing structural issues which would have a long gestation period.

"The risk of subdued economic growth arising from heightening financial market volatility, rising protectionism and escalating trade tension could be a further blow to the Malaysia property market in 2019," it says in a recent report.

The research house says the concern of large property overhang has become more alarming since 2018 as the data from the National Property Information Centre has been registering a consistent uptrend.

"We believe 2019 could see the peak of property overhang as the heavy completions from 2016 to 2018 take their toll on the supply factor, reflecting the subdued property price growth.

"This unprecedented large property overhang will probably take a long gestation period for the market to absorb the new supply before the sector could stage a meaningful recovery."

AllianceDBS Research says the new completions from 2016 to 2018 have largely been the culprit for the large accumulated property overhang which is unlikely to be resolved in the near term.

"While the growth in near-future supply is likely to taper off as developers have adjusted their launch pipeline over the past few years, the large unsold inventory remains the key concern which will continue to drag the market.

"In fact, certain developers have started to make provision for inventory impairment, indicating the dire straits of the existing market environment."

Maybank Investment Bank Research in a recent report said home sales have bottomed out and believes that the property market will recover by the first half of this year.

It said property sales would be boosted by the soon-to be-launched home-ownership campaign, a joint effort between the government and private developers.

Meanwhile, RHB Research says property sales are expected to remain flat in 2019, as many developers remain cautious amid subdued sentiment levels.

Given the sluggish property market outlook, it says most developers would either lower or maintain their sales targets for 2019.

"The low visibility of local and foreign direct investments has not helped to spur market sentiment," the research house says, adding that the bulk of property sales this year is expected to be generated from the affordable segment.

Given the sluggish property market outlook, RHB Research said most developers would either lower or maintain their sales targets for 2019.

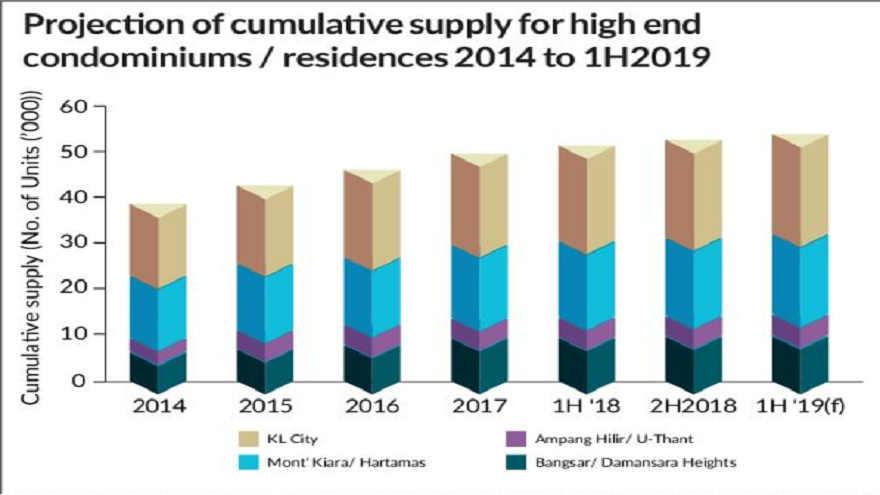

As for the KL high-end condominium market, prices are generally holding firm, says Knight Frank Malaysia in its latest research report "Real Estate Highlights for the Second Half of 2018."

"Looking ahead, the widening gap between supply and demand coupled with rising financing cost will continue to impinge on price growth as the market finds its equilibrium. However, with property developers generally more optimistic about the market outlook, we expect to see more launches moving into 2019 and beyond."

The property consultancy says the slight upward revision in the rates of the real property gains tax and stamp duty announced under Budget 2019 are unlikely to have significant impact on the high-end condominium sector, although the acquisition and disposal costs in property transactions may be higher.

"In contrast, the exemptions and initiatives, in particular the waiver of stamp duty on the instrument of transfer and loan agreement for residential homes valued up to RM300,000 for a two-year period and the six-months waiver of stamp duty charges for properties priced from RM300,001 to RM1mil, are expected to kick-start the housing market moving into 2019 and beyond.

"The introduction of alternative financing through 'property crowdfunding' will further assist first time homebuyers. Although lauded, it is imperative that the innovative financing platform is governed by stringent guidelines across the entire ecosystem to avoid potential sub-prime mortgage crisis moving forward."

Knight Frank Malaysia adds that the recent gazetting of the long awaited KL City Plan 2020 is positive and will provide more clarity to developers and investors alike.

"With improved transparency and accountability in the new government, the outlook for the KL high-end condominium market remains one of cautious optimism with window of opportunities for recovery in the mid to longer term."

AllianceDBS Research meanwhile says high-rise properties have remained the most vulnerable to price weaknesses, given the large accumulation of unsold units that are mainly concentrated within the three major property hubs, namely the Klang Valley, Penang and Johor.

"KL and Penang property price indices have started to bear the brunt of the supply glut of highrise properties given their high concentration in both areas."

Office market

According to Boyd, Greater KL will become the biggest office market in Asean this year.

"With 123 million sq ft, we are getting very close to Hong Kong's 127 million sq ft. The additional 20 million sq ft due for completion by 2022 will put us in the lead and it could happen this year.

The KL office rentals will remain weak but will be supported by demand from the IT industry, co-working operators, the finance sector and upgraders, generally."

However, Knight Frank Malaysia believes that the office market is expected to remain vibrant in the KL fringe area moving into 2019.

"Due to the influx of new buildings, particularly in the Tun Razak Exchange, occupancy rates in the KL city is expected to decline marginally.

"However, rental rates will continue to hold steady as newer buildings tend to command higher rental rates.

"The trend of co-working and shared services is a sweet spot in the challenging office market environment. Labelled "space as a service", the rising popularity of this market segment is demand driven by freelancers, start-ups and small and medium sized entrepreneurs."

The property consultancy says there will continue to be active take-up by co-working, shared services and IT related industries.

"Dated but well located office buildings such as Menara Weld, Menara Standard Chartered, Menara Maxis and Menara Milenium will reportedly be undergoing repositioning/upgrading works to improve their market competitiveness in terms of rental and occupancy levels.

"The new government's concerted efforts to implement numerous regulatory reforms augur well for the business operating environment and this is expected to be positive for the country's economic and property market performance over the longer term."

Retail market

Boyd says the fourth quarter of 2018 showed a strong retail performance overall, adding that the market is expected to be resilient in 2019 - particularly for the beauty and wellness, accessories and niche grocery trade segments.

"The major malls will still see strong sales turnover and footfall. We also foresee that the next generation of super malls, such as The Exchange at TRX and Pavilion Damansara Heights, will rapidly become major retail destinations when they are completed post-2020."

Knight Frank Malaysia retail leasing and consultancy associate director Rebecca Phan says that while the retail market remains challenging, she points out that malls are taking proactive measures to create new experiences in order to remain relevant.

"For example, Fahrenheit 88 recently welcomed the country's very first pop-up Selfie Museum to create a multi-sensorial experience that matches the contemporary "insta-worthy" trend. With modern shoppers becoming increasingly tech savvy, malls are now banking on the use of social media to attract more patrons."

In a StarBiz report earlier this month, Malaysian Association for Shopping and High-Rise Complex Management past president Richard Chan said retail market is expected to remain flat in the first quarter of 2019, underpinned by steady, yet cautious, consumer spending.

He says the upcoming Chinese New Year festive period in February will help to sustain the sector during the period.

"Performance won't be much better than 2018. But the Chinese New Year festive period will help. Surprisingly big items, such as car sales seem to do doing well. Bookings for the Proton X70 have been encouraging.

"But we are projecting flat growth in the current quarter, as the majority of consumers are still cautious."

According to Knight Frank Malaysia, six new shopping centres and supporting retail components within integrated developments, offering combined retail space of 4.04 million sq ft, are expected to come onstream by the first half of this year.

"Retailers continue to be spoilt for choice. Developers of new and less prominent shopping centres are offering attractive incentives, partnership and short-term tenancies to pop-up retailers to improve occupancy levels.

"Moving forward, we will see the downsizing of hypermarkets as their owners respond to current consumer preference for smaller stores as well as the closure of non-profitable outlets due to changes in domestic retail trends."

Industrial market

Knight Frank Malaysia capital markets executive director Allan Sim anticipates higher level of land banking activities among industrial property developers in 2019.

"This is because strong latent demand continues to be omnipresent especially for industrial properties with high specifications, as occupiers understand the need to jump onto the Industry 4.0 band wagon in order to future-proof their businesses.

"This presents a unique opportunity for developers and investors alike to gain attractive monetary returns by providing end-users with the right products."

Industry 4.0 refers to the paradigm that machines are now able to autonomously adapt and coordinate their tasks to meet human needs.

Moving forward, Sim says he expects to see new large-scale industrial developments taking shape in strategic locations due to robust demand for warehouses.

"For example, the proposed Free Trade Zone in Pulau Indah, which was recently unveiled by the government, is expected to generate interest from manufacturers and logistics operators alike.

"As for established industrial parks, we continue to see redevelopment of debilitated factories into multi-storey facilities as a mean to mitigate high land costs.

"All in all, Malaysia's industrial property sector, which has been the silver lining for Malaysia's subdued property market in recent years, is set to continue its resilience," he says.

Knight Frank Malaysia says the prospects for the Klang Valley's industrial and logistics property market remain positive this year, as more clarity in the policies of the newly elected government unfolds.

"Several measures announced under the recently tabled Budget 2019 will support growth of the industrial sector, especially high-technology industries. The National Policy on Industry 4.0 strives to catalyse growth of key sectors in the realm of electrical and electronics, machinery and equipment, chemicals, aerospace and medical devices.

"It will pave the way for enhanced productivity, job creation and high skilled talent pool in the manufacturing sector."

.png)

.png)

.png)

.jpeg "Sidebox")